The Great Recession of 2008 temporarily shifted public attitudes regarding traditional financial institutions, while diminished public confidence presented opportunities for new actors to court jaded small businesses. Companies like Shopify and Amazon, which initially excelled in fulfilling critical, albeit non-banking small business needs, also started offering financial services — like payment processing, business funding, and credit cards — to their small business customers, reducing traditional banks’ small business market share.

A majority of banks have adopted a defensive stance in response to the fintech revolution, choosing to add fintechs’ services to their portfolios. By Q3 2021, around two-thirds of banks and credit unions had entered into at least one fintech partnership, according to a report from Cornerstone Advisors and Synctera.

These partnerships have clear benefits for fintechs: Banks shoulder a crushing regulatory burden, sheltering their fintech partners while the fintechs grow their brands. But the partnerships have created a disjointed offering for banks, in which these services are delivered and supported by multiple vendors. What’s more, the revenues resulting from these partnerships have been underwhelming.

Only 28% of the banks and credit unions surveyed by Cornerstone reported that their fintech partnerships had helped increase their loan volumes by more than 5%. A mere 14% reported gains of 5% or more in new product and service revenue derived from their fintech partnerships.

These lackluster results indicate that simply adding siloed services to a bank portfolio is not an optimal approach.

To improve the outcomes of these partnerships, banks need to switch their mindset from a defensive game of checking boxes and accumulating fintech services to intelligently embedding small business management and banking features on a unified platform for their customers.

Changing attitudes

The best-of-breed approach — i.e., using a variety of providers for different services — has an understandable appeal for many SMEs. Theoretically, consuming category-leading products or services through unrelated vendors and financial service providers yields the optimal business value or cost justification.

But countless conversations I’ve had with small business stakeholders all converge on the same point: They’re tired of financial and operational fragmentation, and they want to scale back the number of vendors and financial partners they work with. Why?

There’s no substitute for perspective

Small businesses need financial advisors who are positioned to offer holistic guidance. But sound financial advice requires a complete and holistic view of a business’s current operations, financial health, and development prospects.

Fintechs are too narrowly focused on the specific services they offer to provide small businesses with meaningful consultation, while banks lack insight into their day-to-day business activities.

When business management and financial services are detached and fragmented, none of the individual service providers see the full business picture and are able to deliver optimal advice to their customers.

There’s no substitute for simplicity

Pursuing separate solutions for each business and financial need has left SMEs with a disconnected, ungainly collection of apps. In 2023, small businesses used an average of 80 SaaS apps each. But the slight competitive advantage that each individual app offers isn’t worth the collective headache caused by managing a multitude of credentials and silos.

The desire to pare down vendors extends to financial services as well. In a 2020 Bluevine survey, 87% of U.S. small business owners indicated a preference to receive their banking and credit services from the same financial institution, with 64% finding it “very or extremely important.”

Are banks ready to capitalize?

When I engage with vcita’s customers to better understand their pain points, access to capital repeatedly emerges as a foremost concern. And it’s a service area where banks continue to be outpaced by fintechs.

Many of the SME customers I spoke with have acknowledged to me that when they need capital their primary bank is at the bottom of their target list for a loan. Past experiences give small businesses the accurate impression that they’re unlikely to pass their primary bank’s underwriting process simply because the bank’s records hold very little relevant data.

One of my customers showed his primary bank evidence of significant client order commitments to back his loan request, but his application was met with an apologetic decline. The bank rep told him that she would be happy to approve the loan based on what she saw, but the presented data points weren’t within the bank’s standard lending criteria. She then whispered to him that this happens repeatedly with other small business loan applicants, and she recommended an alternative lender that her SME customers rely on for capital.

Lack of relevant data prevented that bank from generating a new loan product, and in an effort to maintain good relations with its customer, the bank referred the customer to the competition. Stats confirm that this experience is a pattern and not an anomaly: The loan approval rate for alternative lenders in the SME market is more than double that of big banks and 55% higher than small banks.

Banks are equally frustrated by their inability to meet their SME customers’ funding needs. They routinely convey to me that, while they realize the SME market is an enormous opportunity, they don’t have the necessary data sources in place to vet an SME and properly assess its actual risk profile.

In order to re-assume their traditional role as trusted financial advisors for their small business customers, banks need to find ways to learn more about these customers and their businesses.

A business financial management platform

Banks can address their small business customers’ interests by offering a single platform that covers a broad spectrum of mission-critical business needs — like CRM, invoicing, servicing, scheduling and AR/AP — in addition to fundamental banking services, like checking and savings accounts or lending.

An integrated small business financial management platform provides banks and their business customers with a number of mutual benefits:

A productivity platform

When employees use an all-in-one business financial management service, they spend less time repeatedly logging into different apps and repopulating the same data across them. For example, if a business’s customer makes an online payment or taps their credit card in a store, the platform’s app integration automatically updates the business’s accounting software. But if the business uses separate vendors with disconnected solutions for payment processing and accounting, its employees would likely need to manually synchronize the data.

An engagement platform

Customers interact with their bank’s digital assets in a minimal and opportunistic capacity. A recent Accenture study revealed that 63% of consumers primarily use mobile banking just to check their account balance. Small business owners indicate that this figure is quite similar in their case.

By contrast, small businesses frequently and proactively engage with their business productivity apps – every day and between 12 and 20 times per day according to vcita’s own platform usage data.

When a business management platform integrates with core bank services, like their checking balance, or credit card transactions it becomes an asset that a bank’s customers repeatedly engage with. This level of engagement with the bank strengthens the bank’s brand presence, while increasing service consumption and stickiness.

A trusted advisor platform

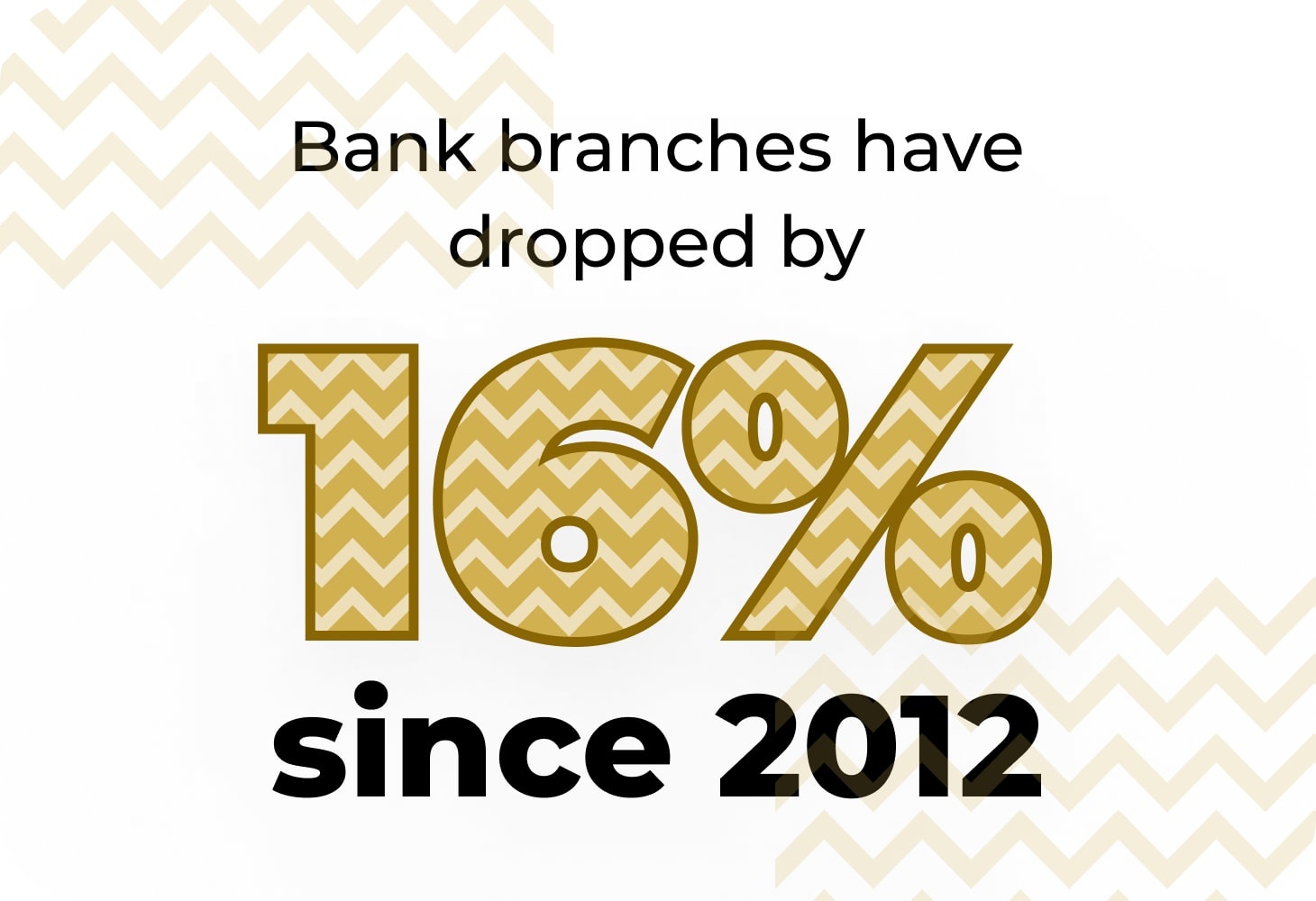

The number of bank branches in the U.S. has dropped by nearly 16% since their peak count in 2012. That reduced emphasis on branch visits has disproportionately impacted the way small businesses interact with their banks – leading to a heavier use of banks’ digital assets. This diminished face time with the bank employees means that they know less and less about their small business customers and are not quite in a position to lend optimal advice.

With the growing importance of the bank’s digital services, the traditional trusted advisor role can be effectively assumed by the bank’s digital platform. With every digital engagement, more and more data about the business is collected, accumulated and synchronized, leading to a more optimized and comprehensive view of the business’ operations – past, present and even future. This allows the platform to intelligently offer insights, recommendations and relevant services to users while they are using the platform to run their business.

Even when customers do end up visiting a physical branch, the bank rep greeting them has direct access to the same holistic view of the business, and is able to immediately assume the traditional trusted advisor role, offering relevant and timely service.

Contextual and more accurate services

The platform’s view of a small business’s day-to-day activities allows banks to contextually identify the relevant services for these customers in real time.

For instance, if a manufacturer gets an unusually large product order, there’s a strong possibility that it will need a capital infusion to buy materials, pay contractors, and rent a bigger production space. When the order is processed through a business financial management platform, that platform can identify the order as an opportunity to immediately prequalify the business for an appropriate loan or line of credit.

Because the platform has an exhaustive view of historical, current and even planned business volume, credit applications can be more accurately prequalified and evaluated by considering the nontraditional, forward-thinking data points that the platform holds – like business volume traction and trend, committed work schedules, approved estimates, invoices, and more.

That omniscience allows a bank to more accurately assess a business applicant’s risk profile than it could have without this data and increases the likelihood that worthy small businesses will receive the funds they would otherwise get elsewhere.

And most importantly, these types of contextual and timely in-platform offers are far more likely to be adopted by customers than if they had been generated randomly and out of context.

Trend-based product development

Operational data across a bank’s entire small business portfolio can be aggregated and anonymized at the platform level, allowing the bank to identify and strategically respond to consumption trends. For example, a gradual spike in high-ticket orders in a specific vertical such as home services, may present an opportunity for the bank to either create a new, or refocus an existing BNPL product for this specific audience in support of their business needs. Such a proactive move, increases the bank’s customer satisfaction and loyalty, while growing revenue.

The leap to an all-in-one platform

Banks are understandably hesitant to provide small business management products that fall outside of the traditional banking wheelhouse. But it’s a necessary evolution on the path toward optimally servicing the small business sector at scale. If banks don’t expand their focus on banking and financial services by rebundling into a complete small business financial management platform, they’ll miss out on this window of opportunity to regain control and reposition themselves as their customers’ trusted financial advisors.

Organically building an in-house business financial management platform is an expensive process that could take banks years to complete. A more viable alternative is selecting an existing, interoperable and already-proven 3rd party platform, and integrating it into both their own organic financial services, as well as their fintech partner services. This ensures an overall service offering that is current, integrated and relevant, without sacrificing control.

A bank could opt to present the new platform under the vendor’s name, but white-labeling it and offering it under the bank’s own brand would create greater trust among its business customers, increase adoption rates and lead to a stronger brand presence. Partnering with an experienced platform vendor is the recommended approach, allowing the bank to benefit from the vendor’s proven track record of delivering and even operating the platform on behalf of its partners.